FHA Mortgages

An FHA mortgage (which stands for Federal Housing Administration) is one of the most popular loans for first time home buyers. This loan is a government sponsored loan program that you may have heard of for its well known 3.5% down payment option. Heres what you really need to know about these loans:

There is no income limit, like in other government loans such as USDA

There is a misconception that these loans are only for low-income or first-time home buyers

Primary occupancy is required

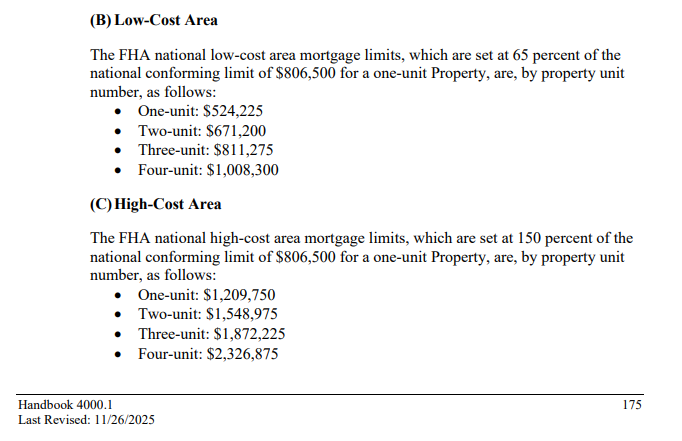

The graphic is directly from FHA Single Family Housing Policy Handbook which is updated just about every year indicating new loan limits

You need to have income to pay the monthly mortgage

580+ Credit score eligible for 3.5% downpayment

500-579 Credit score requires a 10% downpayment

Your debt to income ratio (DTI) will determine how much house you can afford

TOTAL MONTHLY DEBTS / GROSS MONTHLY INCOME

FHA provides mortgage insurace, aka MIP (Mortgage Insurance Premium) which is partially paid upfront 1.75% of the loan that can be financed into the loan and then partially paid in monthly payments

Once your initial application is in for an FHA loan your loan will enter the processing stage. From here the neccessary documents needed such as an ID, recent paystubs, W2/Tax documents …etc will be requested, and the quicker you get that to the Loan Officer, the quicker the process can move along. Just to keep this related to FHA loan we can talk about the home buying proccess in a little bit, we will cover what the underwriter will be looking at to approve your loan. The underwriter is the person that makes the final decision on if your loan will be funded and issue a clear to close. To break it down simply, they look at what is known as the 4Cs:

Credit Your credit history which is their indicator of your willingness to repay debt

Cash Your cash assets available to close the mortgage

Collateral An appraisal will evaluate the value of the home

Capacity to Repay this is your income and employment history. accounting for housing exense and your total DTI

There are many aspects to the FHA loan that can be used to your benefit, the lower downpayments if you qualify, higher DTI limits, theres even a program that combines a home purchase or refinance with renovation costs into one mortgage for primary residences. It is used for repairs, improvements, or upgrading properties; this is called the FHA 203(k) loan.

Simply put, this is an amazing program that makes home buying realistic for everyday people to build weath. You may hear me say that a lot, and the message I am trying to push is YOU CAN BUILD WEALTH THROUGH HOME OWNERSHIP, DON’T LET NOT KNOWING BE THE REASON YOU DON’T.

This is the loan that Dalia and I used back in 2019 to purchase our home, and with a small down payment and completing the marathon to the closing day we have built over $100k in equity. We did happen to buy at the perfect time as this isn’t always the case since the market can fluctuate but even over the course of the loan while you pay down that loan you will have a built in piggy bank which is a wealth building tool that renting does not create. That said, we did get lucky and the market took a huge upswing (for owners) at that time and this is the true testament to it’s not about timing the market, its about time in the market. If you decide this is the right loan for you and your family, I’d be more than happy to pursue this goal with you or discuss other strategies to getting you into your house!