Build Your Credit, Build Your Wealth

A bit after John and I bought our first home, I gained a passion for understanding the Ins and Outs of credit and how to build it. I did many deep dives to understand what we are not taught in school to learn all about what I feel should be a very critical focus point in our education. We’re taught every part of a cell, but we’re not taught many of the basics of adulthood. No matter their age, this is a problem I have personally watched so many people struggle with; they especially realize it when it comes time to buy a home.

Credit Building Tips and Tricks

These are some incredibly helpful tips I have learned over the years through experience, credit specific sites, and Mortgage Loan Officers we have spoken to.

Sources: Centier Bank, Credit Karma, myFICO, Equifax, NerdWallet

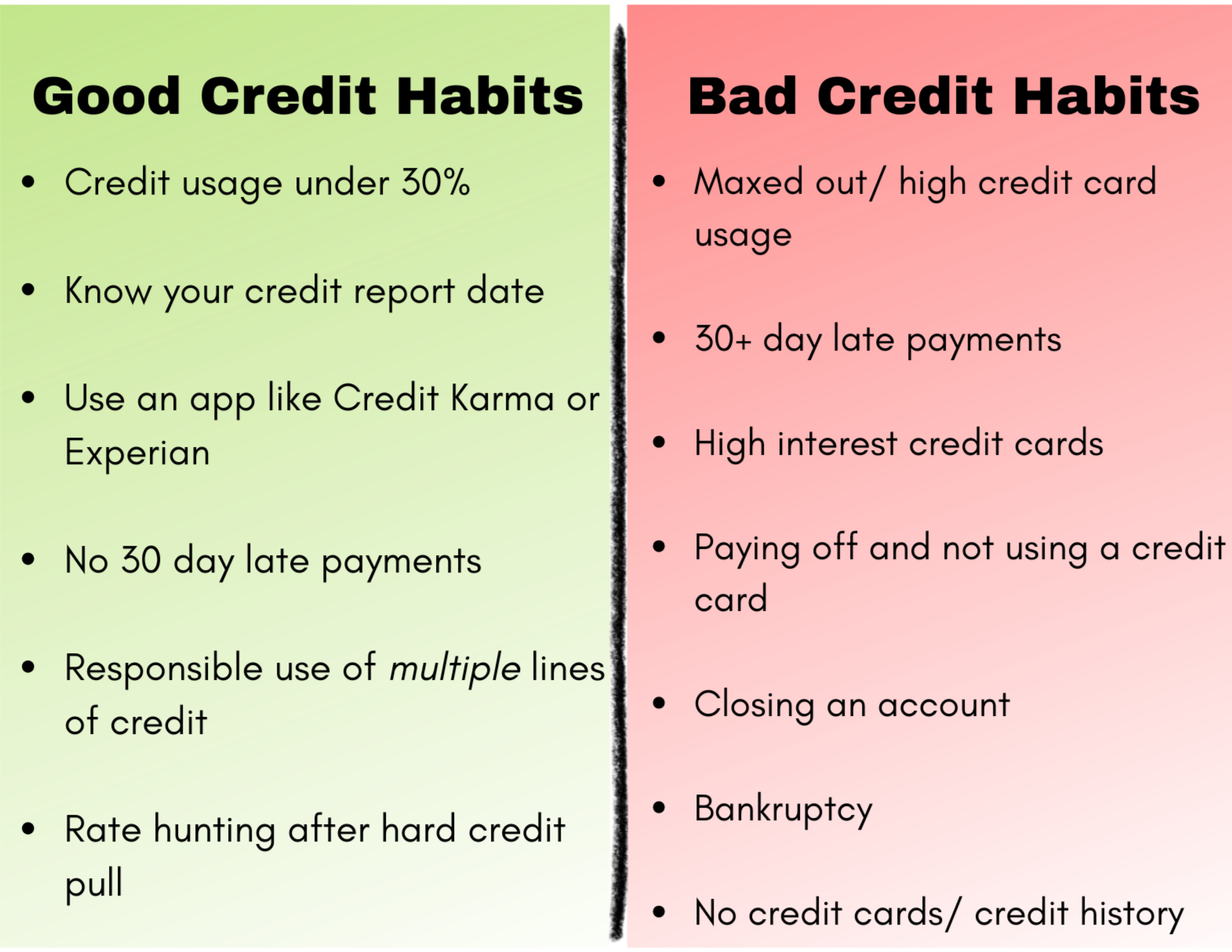

Good Credit Habits:

There are credit usage brackets that change how your credit is scored. 10% or under is ideal, but to have good credit you want to stay under 30% usage. So if your limit is $2500 you want to stay under $750 for 30% usage

Know the day your credit is reported. The day your payment is due matters, however if you make your payment to stay under 30% after your credit is reported, it will not be reported as such. If you pay your card off in full each month, but after that date, it will still report the prior usage. That date is typically the day of the month that you opened your credit card.

Use an app like Credit Karma to keep up with your usage and to get personalized tips to improve your credit. However, you want to keep in mind that this is a rough estimate of your credit score and your credit will likely vary by 20-50 points which is significant for potential approval odds. You get one free credit report every 12 months, that would be the most accurate way to know your score.

A missed late payment stinks, but before the 30 day mark, your only punishment is a late fee. After that, that it is a missed payment reported to the credit bureaus which can significantly drop your credit score and affect your credit for up to 7 years. Though the impact decreases as years pass.

You want multiple lines of credit to maintain a long stable credit history. The longer you have an account open in good standing, the better. Creditors and lenders want to see that they can trust you through your credit history.

One of the most important things you should know, especially if you are reading this because you want to buy a home: You will go through a soft credit check for a pre-approval, that will not affect your credit, but the next step is to get a hard credit check. A hard credit check can negatively impact your credit by around five points. Once you get that hard credit check, you have 14 to 45 days to get as many hard credit checks as you want without any further impact to your credit. This is your time to shop for better rates! Your lender will let you know when your window will close.

Another good tip is to avoid throwing all of your money to paying off your credit cards. As long as you keep your usage under a good low percentage bracket like 10% or 30%, you're good. You are likely to always use your card if there is space. Especially since a card you don't use will be closed on you, which negatively impacts your credit. Plus, Cash Is King. HOWEVER, if you truly are in a credit trap and you want to close your cards, close them! The impact won’t last forever and it will decrease as time goes on. At the end of the day, you need to do what is best for your personal situation.

Bad Credit Habits:

Not being careful of who you co-sign with. This is huge. The person you co-sign with essentially has control of your credit. If your name is on it, you own it. For example: there are far too many stories of people co-signing on a car or a home to help someone with bad credit qualify, where that person ended up delinquent on their payments and now they have a bankruptcy or repossession in their name and on their credit. These can result in a significant drop in your credit score of over 100 points and extreme difficulty in finding loans in the next 7-10 years, especially when it comes to buying a home.

It may sound obvious, but you want to avoid high-interest credit cards. There is nothing worse than being in a credit card trap of always making payments and never making a dent!

Again, missing a payment 30+ days late. Before 30 days will only be a late fee, but 30 days drops your credit score and stays on your credit report up to 7 years.

Paying off and not using your credit card. If you just climbed out of a credit usage hole and are afraid to use your card again, this may seem like a good idea, but an unused credit card will be closed on you after a certain period of time depending on your issuer. A closed account will cause a dip in your credit. The impact depends on the account.

Not having any credit history. You need credit history to build your financial trustworthiness when it comes to anything from renting to buying. You may have good credit, but if your good credit is due to lack of credit history then it won’t be of any help without significant compensating factors.

Biggest credit killers: Missed payments by 30+ days, bankruptcy, and high credit card usage.

“Your credit score is like a report card for your financial health. Make sure you get good grades.”

-Angela Suchecki